Winning government contracts can have a positive impact on a company’s stock price as studied in TenderAlpha’s Government Receivables as a Stock Market Signal white paper.

With that in mind, we thought it would benefit our readers if we offered them analyses of the financial results major U.S. federal government contractors achieve.

Today we will look at a company we have covered previously in our Top Government Contractors series.

Boeing recently reported its Q4 2023 results and below we will provide a brief analysis of the company’s performance discussing its operations, backlog and government contracts exposure.

To read our analyses of Boeing’s results in the previous quarters, please follow the links below:

Part 4: Boeing: Improving Free Cash Flow Generation to Allow Debt Payback (Q4 2022)

Key points:

* 40% of Boeing revenue came from government sources in 2023;

* U.S. government alone accounted for 37% of all company revenue;

* 10% revenue growth in Q4 (2023: +17%), driven by the Commercial Airplanes division;

* Total backlog grew 29% Y/Y to $520 billion at the end of 2023;

* Fixed-price contracts accounted for 58% of Defense, Space and Security revenue in 2023, negatively impacting segment profitability.

Boeing Q4 2023 Results Overview

We last covered Boeing in part 49 of our Top Government Contractors series here. Below we will highlight the progress achieved by the company in Q4 of 2023.

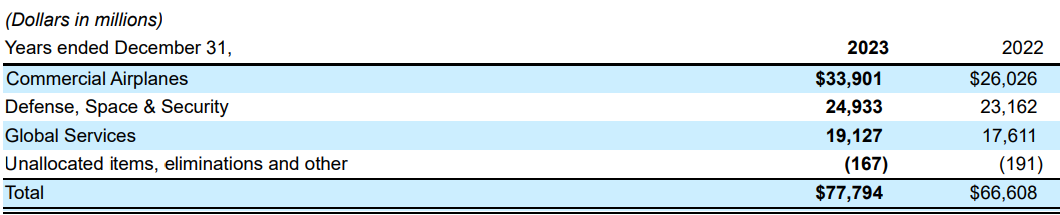

We will start with a Boeing revenue breakdown. The company reports results in three main segments, namely “Commercial Airplanes” (BCA) at 43.6% of 2023 revenues, “Defense, Space & Security” (BDS) at 32.1% and “Global Services” (BGS) at 24.6% of 2023 revenues:

Figure 1: Boeing revenue breakdown between segments

Source: Boeing Form 10-K for Q4 2023

Operational Overview

Commercial Airplanes was the best-performing segment in Q4, growing revenues at 13% Y/Y (2023: +30%). The operating margin was positive in Q4 at 0.4% (2023: negative 4.8%). Despite the Alaska Airlines accident involving a 737 airplane which saw a flight from Oregon to California make an emergency landing on Jan 5, the company continues to deliver airplanes and reinforcing its focus on quality with numerous initiatives.

Defense, Space & Security delivered 9% Y/Y revenue growth in Q4 (2023: +8%). The division continues to suffer from fixed-price contracts, with a negative operating margin of 1.5% in Q4 (2023: -7.1%).

Key Boeing defense contracts awarded during the quarter include a contract from the U.S. Air Force for 15 KC-46A tankers and the start of developmental flight test program for the T-7A Red Hawk. Furthermore, Canada selected the P-8A Poseidon as a multi-mission aircraft.

Global Services delivered the slowest topline growth in Q4, at just 6% Y/Y (2023: +9%). That said, strength in the high-margin commercial segment drove operating margins to 17.4%, in line with the 2023 average. As a result, operating earnings grew 33% in Q4 (2023: +22%).

On a consolidated level, sales increased 10% Y/Y in Q4 (2023 +17%), Core loss per share was $0.47/share in Q4 (2023: $5.81/share), and free cash flow was $4.4 billion in 2023 (2022: $2.3 billion). The core operating margin was positive in Q4 at 0.4% (2023: -2.4%).

Due to the need to focus on operational improvement following the 737 Alaska Airlines accident, the company did not provide a 2024 outlook.

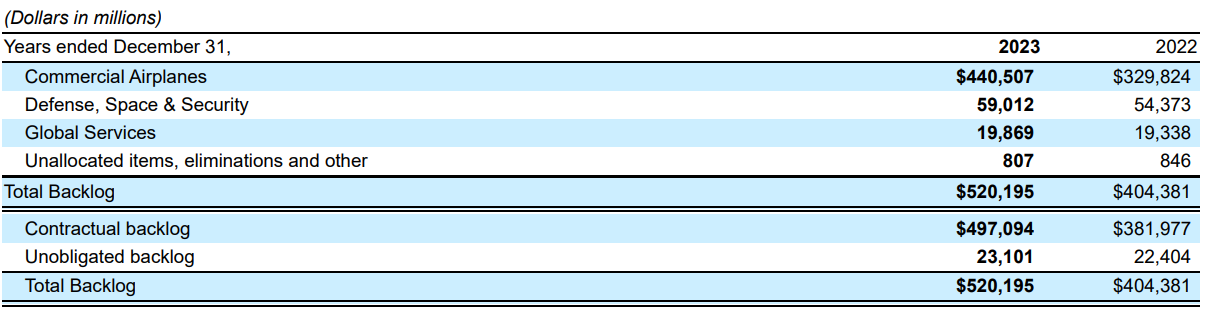

Backlog

Total backlog grew 29% Y/Y to $520 billion at the end of 2023. The bulk of the backlog is in the BCA segment, at 85% of total, or some 5,600 airplanes. Boeing defense contracts backlog, booked in the BDS division, increased 9% Y/Y, reaching 11% of total:

Figure 2: Boeing backlog evolution in 2023

Source: Boeing Form 10-K for Q4 2023

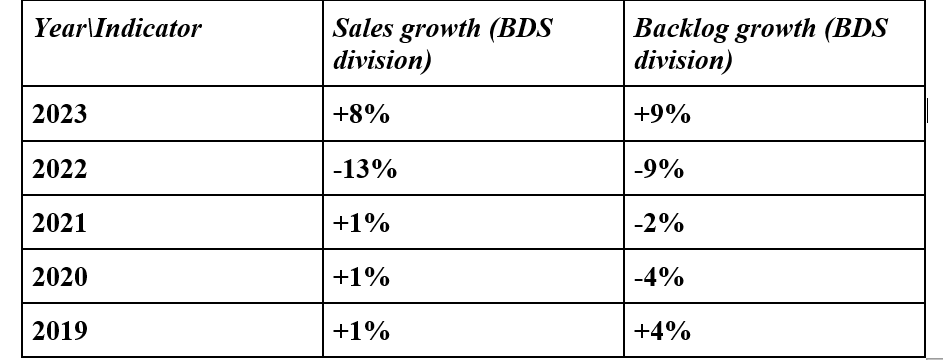

From the data above we can observe that sales in the BDS division (+8% in 2023) have largely kept up pace with the 9% increase in Boeing government contracts backlog. This has largely been the trend since 2019, implying that the key to reducing Boeing’s swelling backlog lies exclusively in the BCA division:

Figure 3: Boeing government contracts: revenue and backlog evolution

Source: Boeing Annual Reports

The table above also shows that 2023 was the first year since 2019 in which Boeing managed to grow its defense contracts backlog. Furthermore, the company noted that at the end of 2023 some 29% of BDS backlog was attributable to non-U.S. customers.

Capital Position

Boeing ended 2023 with a net debt of about $36.3 billion. Against a market capitalization of $128 billion, Boeing remains one of the most levered companies in our Top Government Contractors series. As a result, monitoring Boeing cash flow remains a top priority for both management and investors.

Government Contracts Exposure

Boeing defense contracts account for a substantial amount of Boeing government contracts. Government orders are booked primarily through the BDS division, as well as the BGS services business to a lesser extent.

In 2023, a combined 37% of Boeing revenue came from the U.S. government alone. In addition, foreign governments accounted for an additional 3% of Boeing revenue. As a result, the cumulative government revenue exposure of Boeing was 40% in 2023.

These Boeing government contracts are primarily fixed-price contracts. In 2023, fixed-price contracts accounted for 58% of BDS revenue and 65% of BGS revenue.

The company highlighted in its 2023 10-K report that some $1.6 billion in additional losses were booked on fixed-price contracts of Boeing’s five most significant development programs (Commercial Crew, KC-46A Tanker, MQ-25, T-7A Red Hawk, and VC-25B Presidential Aircraft).

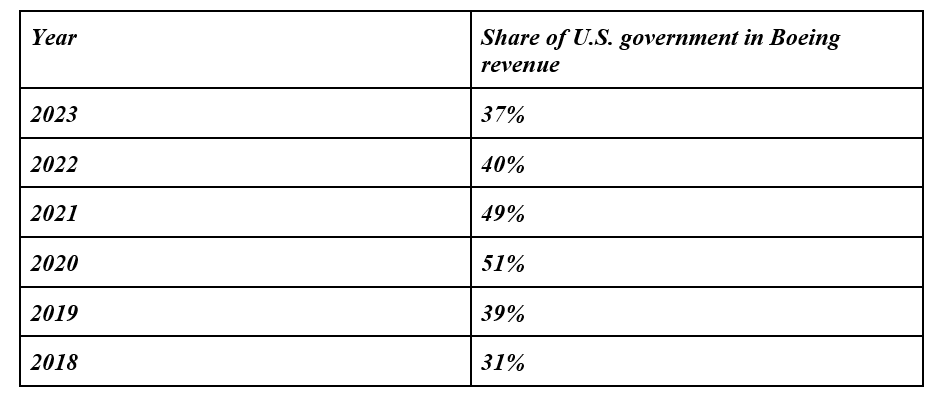

Figure 4: Boeing government contracts evolution

Source: Boeing Form 10-K for Q4 2023/2020

From the data above we see that with the air traffic recovery following the COVID-19 pandemic, the share of U.S. government spending in Boeing’s revenue is approaching normalized levels observed in 2018-2019.

Conclusion

Boeing ended 2023 with a record backlog of $520 billion and a positive operating margin. Boosting production while improving execution quality will be key for the company to reach its $10 billion free cash flow target. The current lack of financial guidance indicates the extreme uncertainty for Boeing cash flow.

The BDS division marked the first backlog increase in 2023, following three years of declining Boeing government contracts backlog. Sales at BDS kept pace with the backlog increase, which has largely been the trend since 2019. Given the prevalence of fixed-price contracts in Boeing defense contracts, margins will only improve gradually at BDS.

The services business represented by BGS remains the slowest growing but most profitable division of the company. As the company works through BCA and BDS backlogs, the BGS division is set to continue growing for the foreseeable future.

Given that 40% of Boeing revenue came from government orders, monitoring the company’s public procurement activity appears to be a smart move that can provide key insights into its financial health.

To learn more about the ways in which TenderAlpha can provide you with insightful public procurement data, get in touch now!

This article was written by members of TenderAlpha's team and does not serve as a recommendation to buy Lockheed Martin or any other stock. TenderAlpha is not receiving compensation for it and we have no business relationship with any company whose stock is mentioned in this article.